“Since the unemployment rate in the Republic is of concern to Government; and since Government recognises the need to share the costs of expanding job opportunities with the private sector…” (Preamble to the Employment Tax Incentive Act 26 of 2013 [ETI Act])

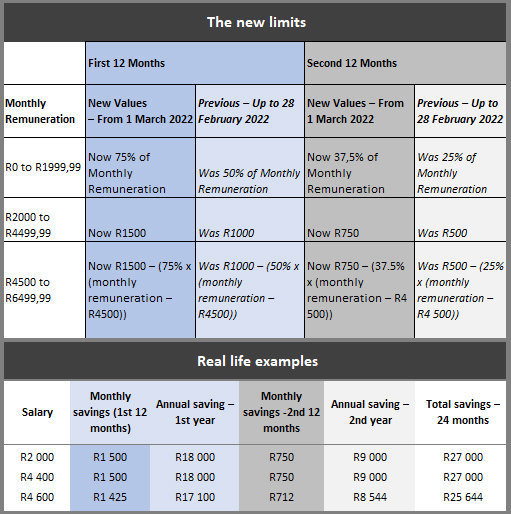

During Finance Minister Enoch Godongwana’s 2022 Budget Speech, a substantial 50% increase in the limits for the Employment Tax Incentive (ETI) was announced, effective from 1 March 2022. This will increase the amount of tax relief employers can claim when employing young people.

ETI fast facts

- An incentive encouraging employers to hire young work seekers aged between 18 and 29 years.

- Reduces the employer’s cost of hiring young people through a cost-sharing mechanism with government.

- Can be claimed for a 24 month period for all employees who qualify.

- Came into effect on 1 January 2014 and will end on 28 February 2029.

- ETI is claimed by reducing the amount of Pay-As-You-Earn (PAYE) due by the company, leaving the wage received by the employee unaffected.

As the monthly remuneration increases, the amount of the rebate reduces: at the upper limit with a monthly remuneration of R6 400, the monthly rebate is R750.

Even so, especially for companies with many employees, these rebates will add up on a monthly basis, and stack up over two years. There is no limit to the number of qualifying employees that you can hire.

Pitfalls to be aware of

- Beware the qualifying criteria

- Employers must meet the qualifying criteria on an ongoing basis, including being registered for Employees’ Tax (PAYE) and being tax compliant.

- Employees must meet the qualifying criteria on an ongoing basis, including having a valid South African ID or permit; be between 18 and 29 years old; earning between minimum wage or R2 000 and R6 500 for a 160-hour month; and who is not a domestic worker or a “connected person” to the employer.

- Beware the continuous changes

- The value of the ETI is not static but depends on the value of the monthly remuneration paid to the qualifying employee, and must be calculated each month for each qualifying employee. In addition, if a qualifying employee worked less than 160 hours in the month, the value of the ETI must be calculated proportionally.

- The ETI is constantly being refined, expanded and tightened – including a series of amendments to the ETI Act with effect from 1 March 2022, so employers claiming ETI must stay updated to ensure they remain within the bounds of the ETI Act.

- Beware the deadlines

- If all the allowable ETI wasn’t used at the end of each six-month reconciliation period (1 March – 31 August and 1 September – 28 February), employers may be refunded the amount, if they are fully tax compliant.

- A non-compliant employer will have until the end of the next reconciliation cycle to correct any non-compliance and be able to receive the ETI refund. If the employer doesn’t become compliant by the end of the next six-month reconciliation period, the ETI refund will be forfeited.

- Beware the possible penalties

- Penalties equal to 100% of the ETI claimed will apply when an employer claims the ETI for any employee who does not qualify.

- Penalties imposed will result in under-payment of employees’ tax, which could result in possible interest and penalties in terms of the Tax Administration Act.

- A penalty of R30 000 will be levied for each employee displaced to employ an employee who qualifies.

- It has been proposed that the ETI Act be amended to impose understatement penalties on reimbursements that are improperly claimed.

- Beware the potential of audits

- A number of taxpayers have faced time-consuming and costly verifications and audits of their ETI claims.

- Additional assessments issued by SARS may reverse the ETI initially claimed by employers.

- Recordkeeping is required by the ETI Act.

- Beware of potential scams

- Employers should exercise vigilance regarding tax abusive ETI schemes and scams offered by third parties, as the employer would carry all the risk in respect of the tax and labour obligations.

Seek professional assistance to ensure you can navigate all these potential pitfalls and claim this ETI incentive, so you can employ more young people while sharing the cost with government.

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© CA(SA)DotNews