“This is a call for all South Africans to be part of the solution; to contribute in whatever way they can to ending energy scarcity in South Africa.” (President Cyril Ramaphosa)

For more than a decade, local businesses have faced the huge challenge of an unreliable power supply from a state-owned monopoly that allowed very little in terms of affordable or practical alternatives.

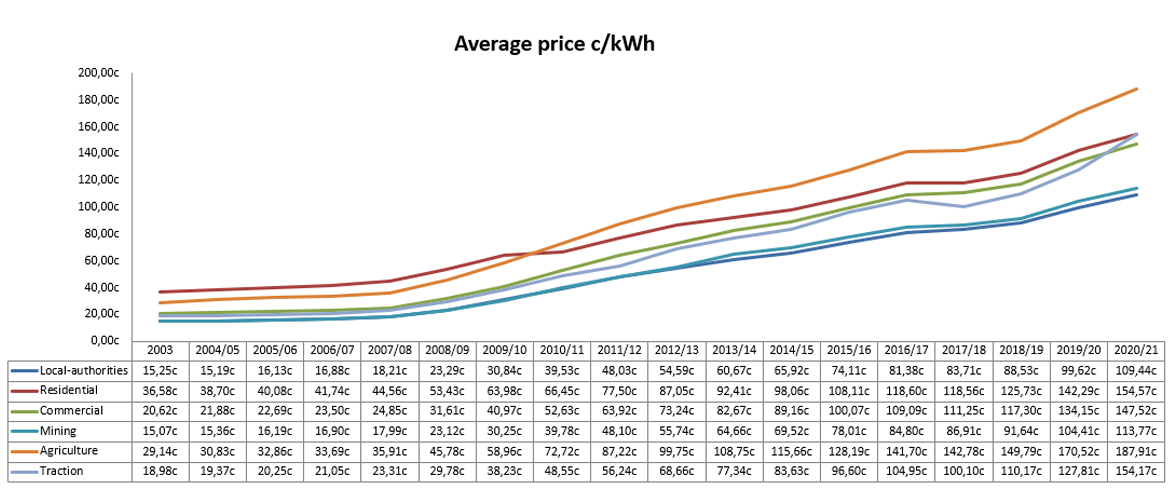

In addition, since then Eskom’s electricity prices continued to skyrocket – increasing by more than 400%.

Click here to view | Source: Eskom Distribution

Just a month ago, Eskom proposed a further tariff increase of 32.7% to the National Energy Regulator of South Africa (Nersa) and is also contesting, in court, the tariff increase of 9.6% for 2022/23 Nersa allowed, which was far below the 20.5% requested.

A national crisis

South Africa’s energy crisis has been described as the biggest risk to the country’s economy. Recently President Cyril Ramaphosa, in his address to the nation on the energy crisis, announced measures to tackle it, including scrapping the licensing threshold of 100MW, Eskom buying more electricity from existing independent power producers, importing power from Botswana and Zambia, and doubling the amount of renewable generation capacity procured through Bid Window 6.

Of particular interest to businesses and individuals are the measures designed to enable businesses and households to invest in rooftop solar.

“South Africa has great abundance of sun which we should use to generate electricity. There is significant potential for households and businesses to install rooftop solar and connect this power to the grid,” the President explained. “To incentivise greater uptake of rooftop solar, Eskom will develop rules and a pricing structure – known as a feed-in tariff – for all commercial and residential installations on its network. This means that those who can and have installed solar panels in their homes or businesses will be able to sell surplus power they don’t need to Eskom.”

This certainly provides reasons for companies to re-assess the long-term viability of alternative energy sources, particularly photovoltaic (PV) solar energy projects, which are incentivised because of their low impact on the environment and our scarce water resources.

In particular, the President called on businesses to:

- seize the opportunities that have been created and invest in generation projects

- reduce consumption through greater energy efficiency.

The good news is that there are tax incentives to assist in achieving these national priorities.

Section 12B of the Income Tax Act provides for capital expenditure deductions for assets used in the production of renewable energy and particularly incentivises the development of smaller solar PV energy projects with an accelerated capital allowance of 100% in the first year for solar PV energy of less than 1MW.

Section 12U of the Income Tax Act provides for capital allowances for roads and fencing used in the generation of electricity.

Section 12L of the Income Tax Act is aimed at directly incentivising investments in local energy efficiency projects and provides a deduction for actual savings resulting from a reduction in energy use.

Capital expenditure deductions (S.12B)

Section 12B provides for a 50%/30%/20% income tax deduction over three years for certain machinery or plant – which means 50% of the costs of the assets can be deducted in year one, 30% in year 2, and 20% in year 3. These assets must be owned by the taxpayer, brought into use for the first time by the taxpayer, for the generation of electricity from, amongst others, photovoltaic solar energy or concentrated solar energy. The tax deduction also applies to any improvements to the qualifying plant or machinery that are not repairs related.

The following types of renewable generation projects may benefit from the allowance:

- wind power;

- photovoltaic solar energy;

- concentrated solar energy;

- hydropower (producing less than 30 megawatts); and

- biomass comprising organic wastes, landfill gas or plant material.

In respect of photovoltaic solar energy of less than one megawatt, a 100% income tax deduction is allowed in the first year of use.

What this means is that the cost related to a new solar power system can be deducted as a depreciation expense– reducing the income tax liability. The reduction can be carried over to the next financial year as a deferred tax asset.

In a previous binding ruling, SARS confirmed it will allow for both the capital cost of solar power units, as well as the direct cost of installation or the erection thereof.

The capital costs that may be deducted are:

- Photovoltaic solar panels;

- AC inverters;

- DC combiner boxes;

- Racking; and

- Cables and wiring.

In addition, related allowable costs of installation are:

- Installation planning expenses;

- Panels delivery costs;

- Installation expenses; and

- Installation safety officer costs.

Taxpayers installing assets used in the production of renewable energy, and particularly smaller solar PV energy projects or systems should investigate the tax benefits of Section 12B, particularly now that selling electricity back to Eskom will soon be a reality.

Capital allowances for roads and fencing (S.12U)

Section 12U provides for capital allowances for roads and fencing used in the generation of electricity greater than 5MW from wind; solar; biomass comprising organic wastes, landfill gas or plant material; and hydropower to produce more than 30MW. It is granted in full in the year of expenditure and covers improvements to the roads and fencing related to the generation project, as well as foundations or supporting structures.

Energy-efficiency incentive (S.12L)

Section 12L, read with the Regulations, allows any person or entity registered with the South African National Energy Development Institute (SANEDI) to claim a deduction for energy-efficiency savings derived from activities performed in the carrying on of any trade.

The incentive allows for a tax deduction for all energy carriers (not just electricity, but also fuel) but with the exception of renewable energy sources.

Ownership of energy-efficient machinery and equipment is not a requirement to claim a deduction under section 12L, so a lessee of the machinery or equipment can equally claim a deduction under section 12L.

The deduction is calculated at 95 cents per kilowatt hour or kilowatt hour equivalent of energy-efficiency savings and can create or increase an assessed loss.

A taxpayer must comply with certain requirements before being eligible for this deduction, for example, taxpayers are required to register with SANEDI, and a measurement and verification professional belonging to an accredited measurement and verification body must be appointed. An energy-efficiency performance certificate must be obtained from SANEDI detailing the energy-efficiency savings generated for the year of assessment.

Examples of energy-saving measures include, for example, investing in more efficient technologies such as LED lighting; installing clear acrylic door refrigeration equipment to reduce energy consumption in retail stores; using recycled waste heat from refrigeration plants or furnaces to reduce another electrical heating load; or investing in energy savings solutions for HVAC and refrigeration.

With this incentive, businesses can ensure their energy efficiency measures not only result in lower energy costs but also reduces their tax liability.

When heeding the President’s call to invest in generation projects and reduce consumption through greater energy efficiency, businesses and individuals are well advised to investigate further the tax incentives and rebates available. These are complex, so seek professional advice!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© CA(SA)DotNews